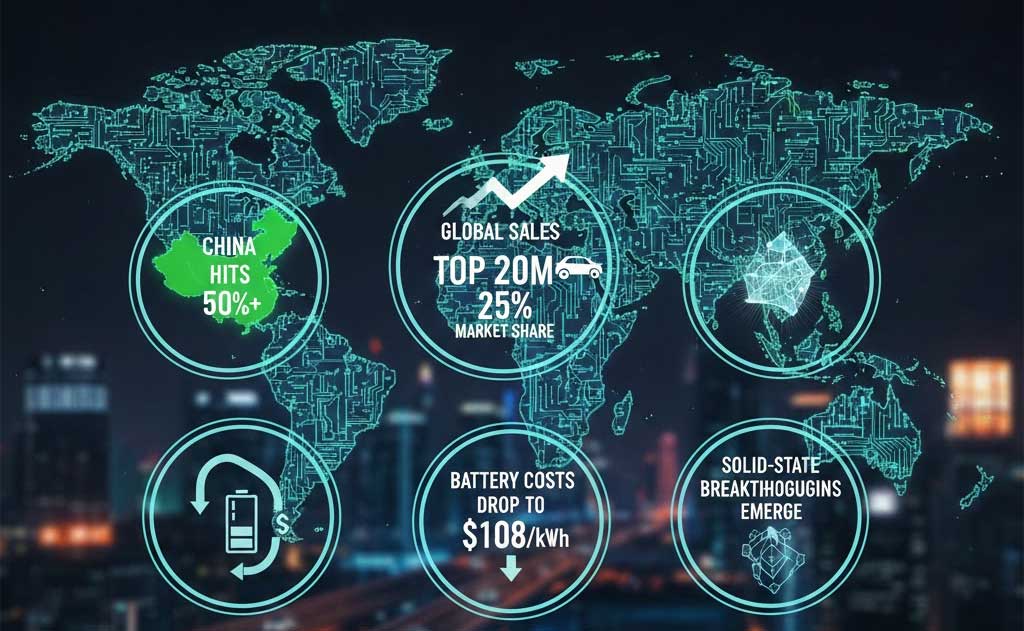

EV trends 2025 recap: Global sales top 20M with 25% market share, China hits 50%+, battery costs drop to $108/kWh, solid-state breakthroughs emerge amid affordability tipping point

It’s December 27, 2025, and the electric vehicle revolution has officially hit escape velocity. Just weeks ago, the IEA’s Global EV Outlook confirmed what insiders suspected: over 20 million EVs sold worldwide, pushing market share to around 25%—a milestone once eyed for 2030. China crossed 50% EV penetration domestically, Europe surged to 25-33%, while emerging markets like Thailand and Indonesia leapfrogged the US in adoption rates.

Here’s what most people get wrong: They think policy flip-flops killed momentum. The number that actually matters is resilience—battery pack prices plunged to a record $108/kWh (BloombergNEF December 2025), solid-state prototypes hit labs and pilots, and charging networks exploded. What this means in plain English: EVs aren’t a niche anymore; they’re the default path, with ICE sales in terminal decline and projections showing EVs at 40-60% globally by 2030.

In this countdown, we rank the seven pivotal shifts of 2025 that sealed the deal for the electric vehicles future and global EV market 2025.

#7: Autonomous Driving Reality Check

Waymo Dominates, Tesla Catches Up Slowly

Waymo expanded unsupervised robotaxis to multiple cities, logging millions of driverless miles and 90%+ crash reductions. Tesla launched supervised Robotaxi tests in Austin/SF but lagged years behind, with FSD v14 updates improving yet still requiring monitors.

Surprising fact: Waymo completed over 14 million paid trips in 2025 (company data).

Contrarian take: Tesla’s vision-only scales cheaper long-term, but 2025 proved multi-sensor (Waymo) wins safety/deployments now.

Rhetorical question: If unsupervised autonomy arrives 2026-2027, who monetizes first?

#6: EV Startups – Survivors vs. Casualties

Shakeout Leaves Few Standing

Dozens failed: Canoo bankrupt, Fisker liquidated, Lordstown/Nikola faded. Survivors: Rivian (VW partnership), Lucid (premium push).

Surprising stat: Hundreds of Chinese startups collapsed; only ~100 remain active (McKinsey 2025).

Balanced view: Consolidation strengthens leaders like BYD/Tesla.

By 2030 expect: <50 Chinese brands dominate.

#5: Charging Infrastructure Wars Intensify

Networks Explode Globally

Public ports grew 30%+ to millions; China added ultra-fast hubs, Europe hit AFIR mandates, US lagged post-incentive but added fast ports.

Surprising fact: China ~65% global chargers; fast chargers surged to 1.6M (IEA 2025).

Projection: 9x growth needed by 2030 for support.

#4: Solid-State Battery Breakthroughs Emerge

Prototypes Promise Game-Changing Density

Factorial/Stellantis validated 375Wh/kg cells; QuantumScape scaled production; Toyota/Huawei patents hinted 500+Wh/kg.

Surprising stat: Energy density doubles lithium-ion potential.

Yes, but… Commercialization slips to 2027-2028.

Rhetorical question: Will solid-state unlock 600-mile ranges affordably?

#3: EV Affordability Tipping Point

Prices Approach/Beat ICE Parity

Battery costs $108/kWh drove sub-$30k models; China achieved SUV parity, Europe/US neared via incentives/deals.

Surprising fact: Used EVs averaged near gas car prices (Cox Automotive).

What this means: Mass adoption accelerates without subsidies.

#2: Tesla Evolves Beyond Cars

Robotics, Energy, Autonomy Drive Value

Optimus prototypes deployed factories; energy storage margins soared 30%+; FSD v14 neared unsupervised.

Surprising stat: Energy became profit engine amid EV competition.

Contrarian: BYD overtook Tesla BEV sales, but Tesla’s AI moat widened.

#1: China’s EV Dominance Solidifies

50%+ Domestic Share, Export Flood

11-12M sales, ~60% global; exports surged, pushing emerging markets ahead.

Surprising fact: China 2/3 global sales; over 50% new cars electric (Ember/IEA 2025).

Data hooks: Global 20M+ sales (25% share); batteries $108/kWh; ICE decline accelerates to 40% EV by 2030.

Future Outlook: Irreversible Momentum into 2026

By 2026: Unsupervised robotaxis scale (Waymo/Tesla); affordable sub-$25k models flood; charging gaps close.

Actionable takeaways:

- Buyers: Hunt deals—parity here.

- Investors: AI/robotics plays (Tesla/Optimus).

- Legacy OEMs: Accelerate or hybrid bridge.

- Policymakers: Infrastructure over incentives.

- Everyone: Transition inevitable—embrace.

2025 crossed the point of no return. EVs lead; future electric.

FAQ

Global EV sales 2025? Over 20M, ~25% market share (IEA/BloombergNEF).

China EV share 2025? Over 50-60%.

Battery cost 2025? $108/kWh average pack.

Solid-state batteries when? Pilots 2025; production 2027+.

EV cheaper than gas 2025? Parity/near in many segments, especially China.

Autonomous status 2025? Waymo leads unsupervised; Tesla supervised scaling.

Top EV startups surviving? Rivian, Lucid; many failed.

Charging growth 2025? 30%+ public ports added globally.

ICE decline projection? EVs 40%+ by 2030; ICE sales peak passed.

Tesla 2025 highlights? Energy boom, Optimus, FSD progress.

I’m Ethan, and I write about the tech that’s actually going to change how we live — not the stuff that just sounds impressive in a press release. I cover AI, EVs, robotics, and future tech for VFuture Media. I was on the ground at CES 2026 in Las Vegas, walking the show floor so I could give you a real read on what matters and what’s just noise. Follow me on X for daily takes.

If you found this useful, the best thing you can do is share it with someone who’d actually appreciate it. And if you want more like it, we’re here every week.

Leave a Comment